Printable Promissory Note Form for Wyoming

Printable Promissory Note Form for Wyoming

The Wyoming Promissory Note form is an essential financial document that outlines the agreement between a borrower and a lender. This form serves as a written promise from the borrower to repay a specified amount of money, along with any agreed-upon interest, within a set timeframe. Key elements of the form include the names and addresses of both parties, the loan amount, the interest rate, and the repayment schedule. Additionally, it may specify the consequences of defaulting on the loan, ensuring that both parties understand their rights and obligations. This clarity helps prevent misunderstandings and provides a legal framework for the transaction. By using the Wyoming Promissory Note, individuals and businesses can protect their financial interests while fostering trust in their lending relationships.

Filling out a Wyoming Promissory Note can seem straightforward, but many individuals make common mistakes that can lead to confusion or even legal issues down the line. Understanding these pitfalls can help ensure that the document serves its intended purpose effectively.

One frequent error is neglecting to include all necessary parties. A Promissory Note should clearly identify both the borrower and the lender. Failing to provide complete names or accurate contact information can create complications if the need arises to enforce the note. It’s essential to ensure that all parties are properly identified to avoid ambiguity.

Another mistake involves the amount being borrowed. Some individuals may write the numerical amount but forget to spell it out in words. This can lead to disputes over the intended loan amount, especially if there is a discrepancy between the two representations. Always include both the written and numerical amounts to provide clarity.

People often overlook the importance of specifying the interest rate. Without a clear indication of how much interest will be charged, borrowers may find themselves facing unexpected costs. It is vital to outline the interest rate explicitly, whether it is fixed or variable, to prevent misunderstandings later on.

Additionally, not stating the repayment terms can lead to confusion. Individuals sometimes forget to include how and when payments will be made. Clearly defining the payment schedule, including due dates and acceptable payment methods, helps both parties understand their obligations and fosters a smoother transaction.

Another common oversight is failing to address what happens in the event of default. A Promissory Note should outline the consequences if the borrower fails to make payments as agreed. This could include late fees, acceleration of the loan, or other remedies. Specifying these terms upfront can help prevent disputes in the future.

Some people may also neglect to sign the document. A Promissory Note is not legally binding without the signatures of the involved parties. Ensure that both the borrower and lender sign and date the document to validate it. This step is crucial for the enforceability of the agreement.

Finally, individuals sometimes forget to keep copies of the signed Promissory Note. It is important for both parties to retain a copy of the document for their records. This ensures that both the borrower and lender have access to the same information should questions or disputes arise later.

By being aware of these common mistakes, individuals can take proactive steps to ensure that their Wyoming Promissory Note is filled out correctly. Taking the time to review the document thoroughly can save both parties a great deal of trouble in the long run.

Transfer on Death Deed Wyoming - The deed must be signed in accordance with state requirements, often necessitating a witness or notarization.

Wyoming Housing Sales Contract - Identifies which party is responsible for closing costs.

The California ATV Bill of Sale form is not only important for recording the sale of an all-terrain vehicle but is also accessible through various resources, including the PDF Templates, which can help streamline the process of completing this essential document with all necessary details and accuracy.

Wyoming Llc Tax Filing Requirements - A foundational document for newly formed corporations.

When engaging in financial transactions, particularly those involving loans, several forms and documents may accompany a Wyoming Promissory Note. Each of these documents serves a specific purpose and helps clarify the terms of the agreement between the parties involved. Understanding these documents is essential for ensuring a smooth transaction.

These documents collectively ensure that both lenders and borrowers have a clear understanding of their rights and responsibilities. Properly managing these forms can help prevent disputes and foster a transparent lending relationship.

When filling out and using the Wyoming Promissory Note form, there are several important points to keep in mind. Here are key takeaways to ensure you understand the process and implications:

By keeping these points in mind, you can navigate the process of creating and using a Wyoming Promissory Note with confidence.

What is a Wyoming Promissory Note?

A Wyoming Promissory Note is a legal document that outlines a borrower's promise to repay a loan to a lender. It includes details such as the loan amount, interest rate, repayment schedule, and any penalties for late payments. This document serves as a record of the agreement between the two parties.

Who uses a Promissory Note in Wyoming?

Individuals and businesses in Wyoming use Promissory Notes. They are commonly used in personal loans, business loans, and real estate transactions. Essentially, anyone who lends or borrows money can benefit from having a clear, written agreement.

What should be included in a Wyoming Promissory Note?

A well-drafted Promissory Note should include the following: the names and addresses of the borrower and lender, the principal amount of the loan, the interest rate, the repayment schedule, any late fees, and the date the loan is due. It may also include provisions for default and remedies available to the lender.

Is a Promissory Note legally binding in Wyoming?

Yes, a Promissory Note is legally binding in Wyoming as long as it meets certain requirements. Both parties must agree to the terms, and the document must be signed by the borrower. It’s important to ensure that the terms are clear and that both parties understand their obligations.

Can a Promissory Note be modified after it is signed?

Yes, a Promissory Note can be modified after it is signed, but both parties must agree to the changes. It’s advisable to document any modifications in writing and have both parties sign the updated terms to avoid confusion later.

What happens if the borrower defaults on the Promissory Note?

If the borrower defaults, the lender has the right to take action as outlined in the Promissory Note. This could include charging late fees, demanding immediate payment of the remaining balance, or taking legal action to recover the owed amount. The specific remedies will depend on the terms agreed upon in the note.

Do I need a lawyer to create a Promissory Note in Wyoming?

While it’s not legally required to have a lawyer draft a Promissory Note, it can be beneficial. A lawyer can ensure that the document complies with state laws and adequately protects your interests. If you’re unsure about the terms or conditions, seeking legal advice is a good idea.

Can a Promissory Note be used for business loans?

Yes, a Promissory Note is often used for business loans. It provides a clear framework for repayment and can help establish trust between the lender and borrower. Just like personal loans, the terms should be clearly defined to avoid misunderstandings.

Where can I find a template for a Wyoming Promissory Note?

Templates for a Wyoming Promissory Note can be found online through legal document websites, or you can consult with a lawyer who can provide a customized template based on your specific needs. Ensure that any template you use complies with Wyoming law.

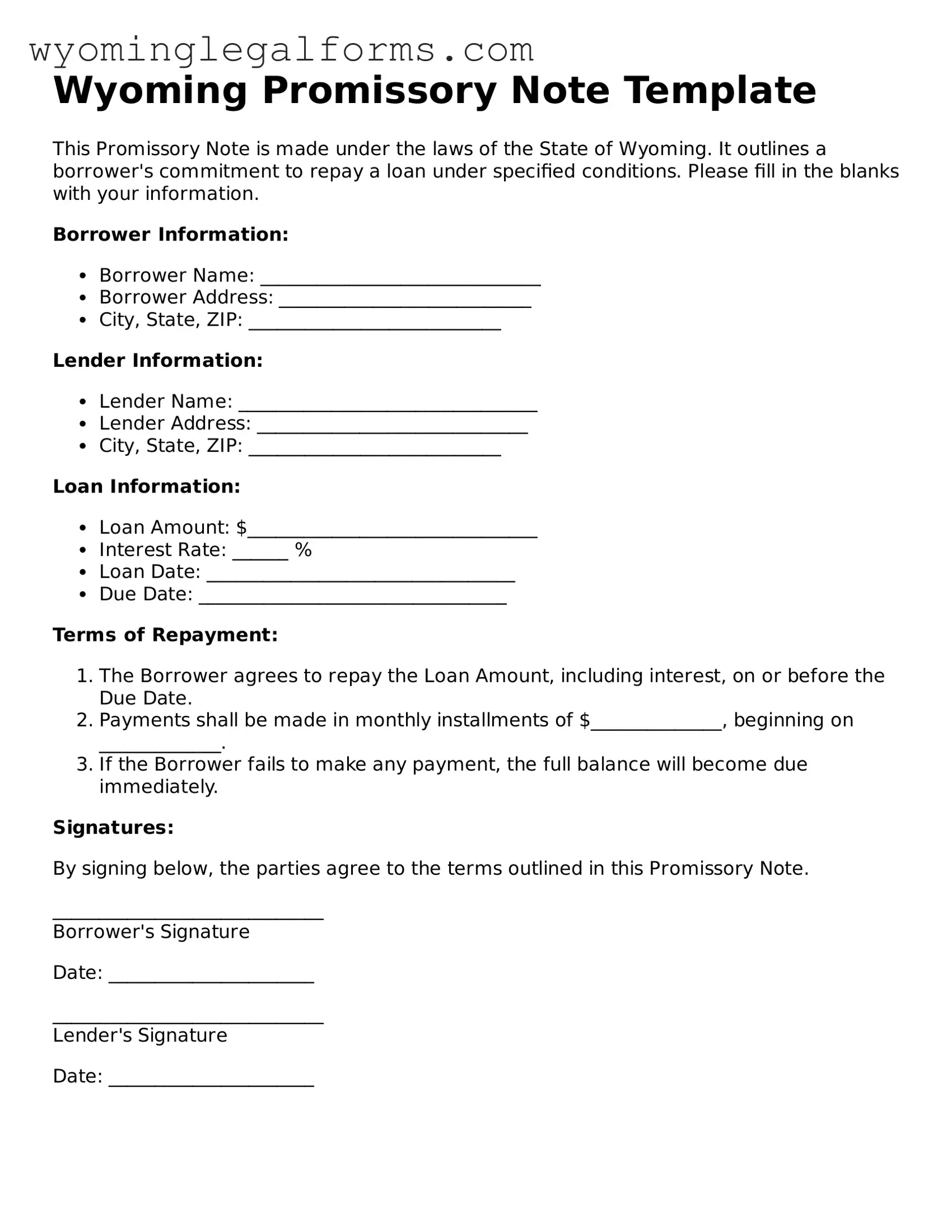

Wyoming Promissory Note Template

This Promissory Note is made under the laws of the State of Wyoming. It outlines a borrower's commitment to repay a loan under specified conditions. Please fill in the blanks with your information.

Borrower Information:

Lender Information:

Loan Information:

Terms of Repayment:

Signatures:

By signing below, the parties agree to the terms outlined in this Promissory Note.

_____________________________

Borrower's Signature

Date: ______________________

_____________________________

Lender's Signature

Date: ______________________

Understanding the Wyoming Promissory Note form can be tricky, especially with the many misconceptions floating around. Here are eight common misunderstandings and the truth behind them.

By clearing up these misconceptions, you can better navigate the world of promissory notes in Wyoming. Understanding the details can save you time and potential legal headaches down the road.